The Ultimate Financial Planning Guide: 2 Types of Money, 3 Statements & 6 Steps

In this article, you'll learn:

What Is Financial Planning?

If you search for “financial planning,” most results will tell you it’s about saving money at a bank, or investing, and maybe a few will mention asset allocation.

But true financial planning is a plan that covers everything from now until the end of your life — including potential marriage, having children, buying a home, buying a car, upgrading your home, upgrading your car, retirement, taxes… and so on.

This plan won’t always keep up with changes, but most people think that simply investing equals financial management. That’s a complete misunderstanding of financial planning.

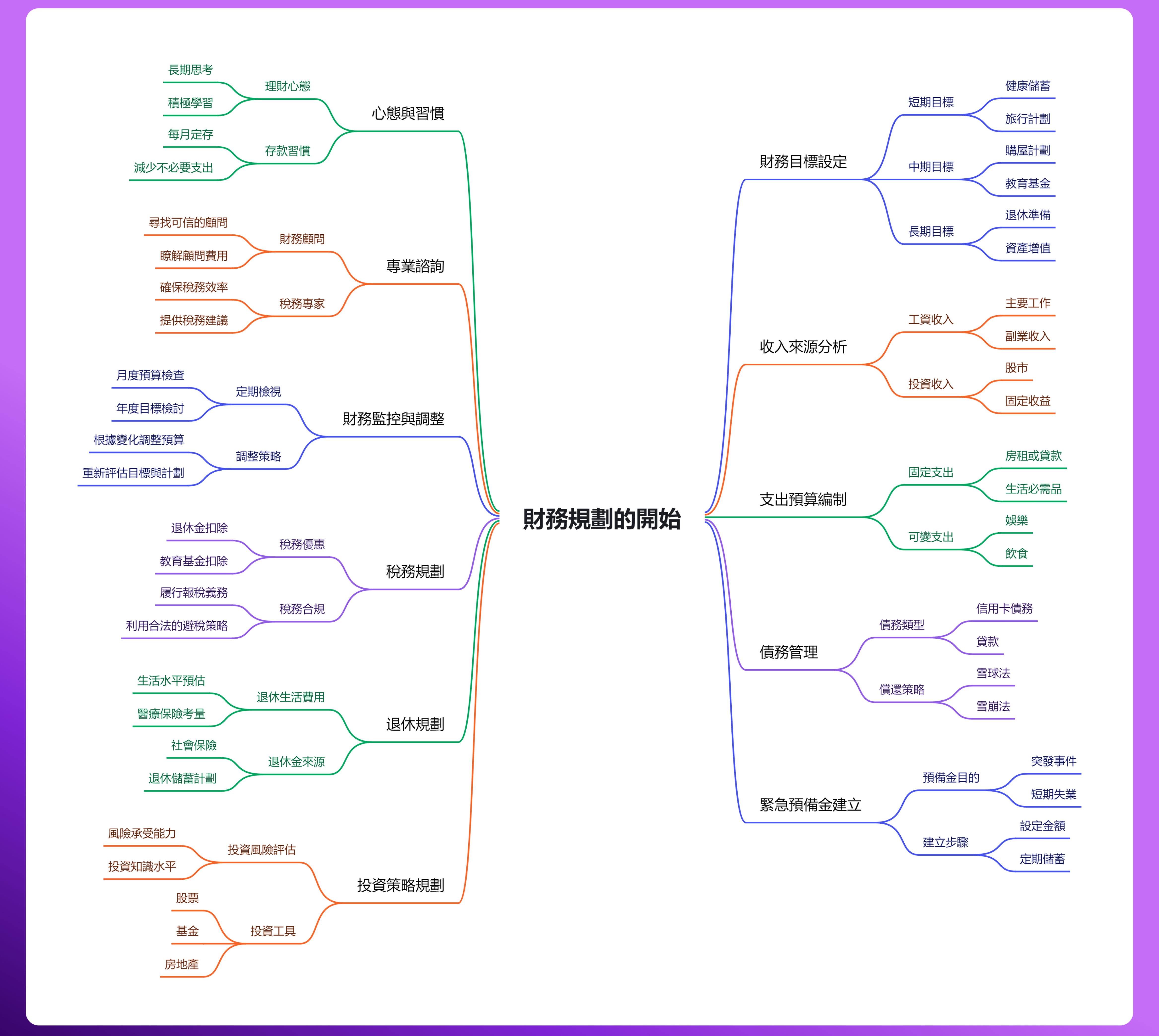

How to Do Financial Planning? 2 Types of Money, 3 Statements, and 6 Steps

Financial planning isn’t just for the wealthy — it’s for anyone who has an income. In this era where earning money is hard but investing is easy, financial planning is an essential skill everyone should master. So how do you go about it? Just master 2 types of money, 3 statements, and 6 steps, and you’ll be off to a great start.

2 Types of Money

Type 1: Income

Whether you’re a part-timer, a salaried worker, or an entrepreneur — anything that flows into your pocket or account is income. This isn’t stating the obvious; you need to first understand the meaning of “money.” Anything that enters your account or pocket is “income.” This includes:

- Full-time job income

- Side gig income

- Parental support income (just kidding… sort of)

- Any other income

All of these count as income. Anything that comes from outside and becomes yours is income — even if you find NT$50 on the street. That counts too. Luck income, perhaps?

Type 2: Expenses

Expenses are the money that flows out of your pocket or account, including:

- Daily living costs

- Housing costs, whether buying or renting

- Transportation costs, whether car payments or public transit

- Investment expenses… and so on.

Wait — did I just say investments are expenses? Yes, that’s right. Anything that’s no longer sitting in your checking account can be counted as an expense, because we’ve converted cash into different assets — that’s a form of spending. (It just shows up differently on the balance sheet.)

Understanding the nature of expenses and then establishing expense principles is a crucial part of financial planning. Only by clearly knowing what your expenses are and why you’re spending can you effectively manage your income and expenses. If you think there are other types of money, check out How to Save Money by Learning to Spend, Not Save

3 Statements

Income & Expense Statement

The income and expense statement is like a diary for your wallet, recording your income and expenses. Simply put, it tracks “where money comes from and where it goes.” Sounds like bookkeeping, right? Don’t worry — unlike traditional bookkeeping, an income and expense statement is more about tracking patterns, not logging every penny. While I don’t personally keep a detailed budget, I do maintain an income and expense statement to visualize my cash flows.

Balance Sheet

The balance sheet is like a wealth record that documents all the assets and liabilities you’ve accumulated from the past to the present. The “spending” mentioned earlier — converting cash into various investment vehicles — has its gains and losses reflected on this statement.

Cash Flow Statement

The cash flow statement is like an EKG for your wallet, tracking the inflow and outflow of cash. It can calculate ratios like your savings rate, insurance expense ratio, living expense ratio, and more, ensuring that within safe ratios, your money is sufficient.

If you want to learn more about these three statements, read: The 3 Essential Financial Statements for Personal Financial Planning

6 Steps

1. Set Financial Goals

First, you need to clearly define your financial goals — such as buying a home, buying a car, saving, or retirement planning. Setting clear goals helps you create a more targeted financial plan.

2. Analyze Your Current Financial Situation

Understand your current financial state, including income, expenses, assets, and liabilities. Only then can you develop a practical financial plan.

3. Establish Income & Expense Principles

Create reasonable income and expense principles to ensure your spending doesn’t exceed your income and that you maintain an adequate emergency fund. This isn’t just about basic bookkeeping — it’s about establishing the right ratios between income and expenses. This may not be achievable overnight. It takes time and adjustments to find a comfortable balance between income and expenses.

4. Mitigate Risks

Using the “right insurance” with “adequate coverage” at a “good premium” ensures that insurance costs don’t become an excessive burden while still providing sufficient protection. This prevents unexpected expenses when specific risks materialize.

5. Asset Allocation Planning

Based on your risk tolerance and financial goals, develop a sound asset allocation plan. Invest for the long term in the stock market, maintain appropriate bond market exposure, and continuously rebalance your assets to ensure your financial goals stay on track.

6. Regular Review and Monitoring

Financial planning always involves “plans not keeping up with changes” — but that’s not a reason to skip planning. It’s like always carrying an umbrella: whether it’s a parasol or a rain umbrella, when it’s sunny you block the sun, and when it’s pouring you block the rain. Regularly review your financial situation, take stock of your financial plan, and adjust based on real circumstances. All of this is to ensure your goals are achieved.

For a deeper dive into the 6 steps: The Basics of Financial Planning: 6 Key Steps to Financial Health and Freedom

Once you’ve mastered these 2 types, 3 statements, and 6 steps, you can start building your own financial plan and take the road toward financial freedom. Remember, financial planning is an ongoing process that requires continuous learning and adjustment to achieve the best results.

Further Reading

Lazy Da’s Conclusion

For someone just starting out with financial management, it can indeed look daunting on paper. It’s easy to feel lost without a clear focus or goal. The moment a well-meaning friend shows up, trust takes over and before you know it, you’ve bought some random financial product.

Remember: everyone’s financial DNA is different. Only you know how your money should be spent. Nobody will scam you — you can only choose to fall for it yourself.

🚀 已有 1,000+ 讀者加入理財成長之路