7 Steps to Financial Planning: Understand Your Money with 7 Key Questions

- 懶大 (Lan Da)

- 財務規劃與心態

- Last updated: September 27, 2023

- 3 min read

In this article, you'll learn:

The 7 Types of Money in Financial Planning

- Earning: Earning money is the first step to acquiring it, including full-time jobs, part-time jobs, etc. You should try any way you can think of to increase your income.

- Allocating: Allocating money means distributing and using the money you earn. Budgeting allows you to allocate funds for savings plans, investment plans, and even fun plans! It’s best to pre-allocate your money on a monthly, quarterly, or annual basis. (It’s not difficult, the hard part is getting started.)

- Saving: Saving money is the foundation for increasing assets. Everyone’s first savings goal should be an “emergency fund,” ideally with 3-6 months’ worth of expenses. Saving money is really not easy. The channels for saving also need to be right.

- Borrowing: There are many ways to borrow money, usually through bank loans, using personal credit or assets to obtain funds. But be careful with your planning to avoid being burdened with debt.

- Spending: Spending money is perfectly fine if it’s within your budget and you have specific goals!

- Protecting: Protecting money refers to transferring risk through insurance, which can reduce financial losses in the event of accidents or illnesses.

- Growing: Growing money, as the name suggests, means making your money grow! Grow your money through compound interest investments. Wouldn’t it be more enjoyable to spend the money you’ve grown?

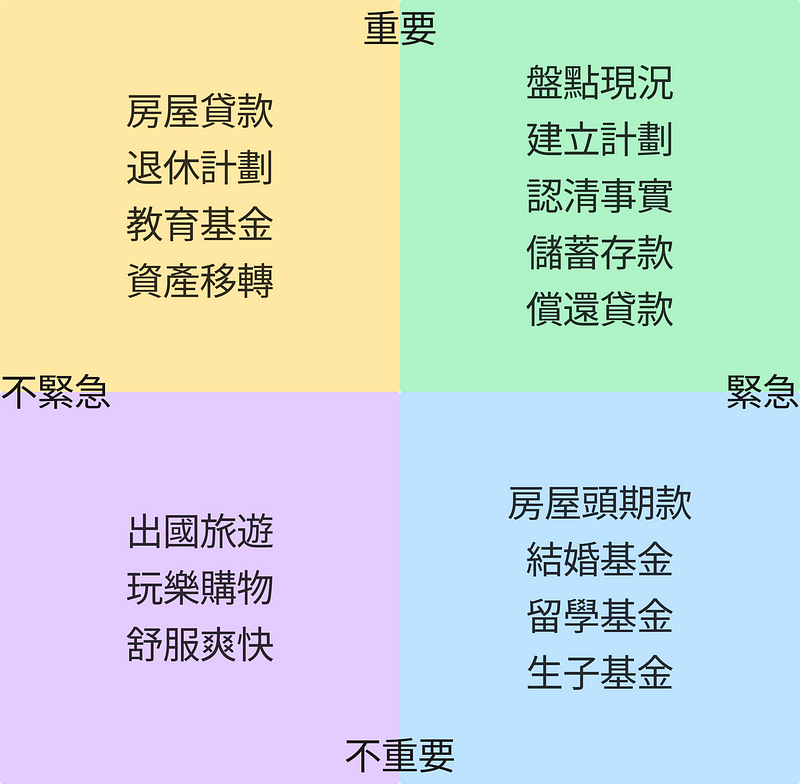

Think About Financial Planning in Terms of Urgent and Important

Important and Urgent

If you don’t have your own financial plan yet, then consciously create one. This plan will turn those non-urgent and non-important things into important and urgent ones!! (Because you know how to allocate resources)

Important but Not Urgent

In financial planning, these things usually become important and urgent over time. For example, a retirement plan. If you don’t start at 20, but start at 30, you’ll miss out on 10 years of compounding.

Not Important but Urgent

Usually, these things in financial planning are more like “imagined” things. It may seem like you need to prepare, but usually it doesn’t happen. It seems like you should save this money, but you don’t necessarily have to.

Neither Urgent nor Important

No explanation needed.

Financial Planning Should Consider Personal and Environmental Factors

Financial planning should also consider personal and environmental factors. Personal factors include your current life stage, occupation, income, family responsibilities, family relationships, and personal values.

External environmental factors include the overall global economic situation, such as recent interest rate hikes, stock market fluctuations, and rising consumer price index (CPI). These economic factors can also affect personal and family financial planning. It’s possible that the basics you originally planned to buy a house with are no longer enough because housing prices have risen too much, so you give up.

Therefore, when conducting financial planning, be sure to assess the impact of personal and environmental factors, incorporate them into your considerations, and maintain sufficient reserves.

Financial Self-Diagnosis or Self-Destruction?

The following 7 questions test whether you have the necessary knowledge and skills for a financial check-up!

1. Do you understand your current financial situation?

- Answer: I know, there’s NT$980 (USD$30) in my account.

- 懶得解釋 (Lazy to explain): Well! Then pray you have a rich dad!

2. Do you know how much money you spend on fixed expenses each month?

- Answer: I don’t know, I forgot how much I spent last month.

- 懶得解釋 (Lazy to explain): This is the typical financial situation of someone who’s always broke.

3. Do you pay your credit card bills on time every month?

- Answer: Yes, I use installment payments on my credit card so I don’t have to pay too much at once each month.

- 懶得解釋 (Lazy to explain): This is the typical financial situation of someone with a “credit card slave” life.

4. Is your monthly income greater than your expenses?

- Answer: I don’t know, I’m too lazy to calculate it.

- 懶得解釋 (Lazy to explain): This is the typical “Buddhist financial management” attitude.

5. If there are sudden expenses, do you have an emergency fund to cover them?

- Answer: No, if there’s an emergency, I’ll borrow money first.

- 懶得解釋 (Lazy to explain): This is the typical financial situation of “living on borrowed money.”

6. Do you have the habit of saving money?

- Answer: No, I think saving money is boring.

- 懶得解釋 (Lazy to explain): This is the typical financial situation of “not wanting to work hard.”

7. Do you know that you have to pay late fees or revolving interest if you pay your bills late?

- Answer: I don’t know, I’ve never paid late.

- 懶得解釋 (Lazy to explain): This is the typical financial situation of “being lucky.”

If your answers are mostly “I don’t know” or “no,” then you probably need a financial check-up.

If you forget all the financial tools, you will succeed in financial management.

Further Reading

懶得變有錢 (Lazy to be Rich)’s Conclusion

🚀 已有 1,000+ 讀者加入理財成長之路